The Lights Are Back On: What San Clemente's Historic Miramar Reopening Means for North Beach Property Values

San Clemente's Miramar Food Hall is finally open after 30+ years. What does a landmark reopening mean for North Beach home values? An appraiser's read.

San Clemente Miramar Food Hall

For more than three decades, the Miramar's marquee sat dark at the gateway to North Beach — a beautiful old building everybody drove past and nobody could get into. As of June 2026, that's finally over.

On June 18, the Miramar Food Hall opened its doors at 1720 N. El Camino Real, bringing life back to one of San Clemente's most recognizable landmarks for the first time since 1992.

As a San Clemente appraiser, I pay close attention to projects like this — not because of the headlines, but because a landmark coming back online is exactly the kind of locational shift that shows up in property values over time. More on that below. First, the story, because it's a good one.

A movie palace built for a young beach town

The building opened in 1938 as the San Clemente Theatre. This was still the early days of Ole Hanson's "Spanish Village by the Sea," and the theater was meant to be a premier coastal entertainment destination — a real movie palace for a town still finding its footing. It was designed by Clifford A. Balch, an architect who specialized in California theaters, in the Spanish Colonial Revival style that gives so much of San Clemente its character to this day.

A bowling center went up next door in 1946, turning the corner into a genuine entertainment hub at the north end of town. In 1969, a major renovation brought new seats, a new marquee, and a new name: the Miramar Theatre. But as multiplexes took over and the economics of single-screen theaters fell apart, the Miramar eventually went dark, closing in 1992.

Then it just... sat there. For over thirty years. Three decades of false starts and red tape. The Miramar didn't sit empty for lack of trying — it sat empty because nearly every attempt to bring it back ran into a wall.

San Clemente Miramar Food Hall

Ownership changed hands repeatedly. Richard Lee bought the theater and bowling alley in 1998 with redevelopment plans that never materialized. A 2005 fire damaged the lobby and restrooms. At one point, owners proposed tearing the whole thing down and replacing it with a four-story mixed-use complex — a plan that drew strong opposition from the San Clemente Historical Society and a coalition of residents, who fought to preserve the building. By then it had been recognized as a local landmark and folded into the North Beach Historic District, which raised the bar for what any developer could do to it.

The city approved a redevelopment plan in 2017 — an events center in the old auditorium and a restaurant food court in the bowling alley. Then construction stalled after a falling-out with the general contractor. The project was resubmitted to the city in 2023. When crews finally got to work on the bowling alley, they discovered the structure was too far gone to save and had to be carefully dismantled and rebuilt, preserving and reusing original materials where they could — including wood from the old bowling lanes that now lives on inside the bar. Even late in the game, in November 2025, a preservationist appeal challenged proposed changes over concerns about the building's historic integrity.

Fire, demolition fights, landmark protections, ownership churn, a contractor blowup, a structure too rotted to stand, and preservation appeals — pretty much the full menu of everything that can slow a project down. That's why actually seeing the doors open feels like a genuine milestone.

What's there now

The Miramar Food Hall opened June 18, 2026, at 1720 N. El Camino Real.

The Miramar Food Hall occupies the 12,600-square-foot former bowling alley building, built around the idea of variety under one roof. It opened with around 14 vendors and is set to grow to 15, plus an indoor bar and an outdoor bar, ocean views, and patio seating.

The lineup leans into range — sushi, Detroit-style pizza, burgers, tacos, Thai, Mediterranean, and more. Vendors include Cosmos Burger, El Puerto Street Tacos, Graciously Thai, Hen Haus, Immersion Coffee Co., It's Allll Rice, La Vida, Lobster Lab, MOTO Pizza, Norigiri, RolledUp SC, Sidelines Sandwiches, and The Pita, among others. Food vendors are slated to run daily from 7 a.m. to 9 p.m., with the bars open from 11 a.m. to 9 p.m. Sunday through Wednesday and until 10 p.m. Thursday through Saturday.

And the food hall is only half the story. The restored theater auditorium next door is becoming the Miramar Event Center, operated by Wedgewood Weddings for weddings and private events, with an opening expected this fall.

An appraiser's read: why a reopening like this matters to value

Here's where it gets interesting from a valuation standpoint.

The Miramar is, in appraisal terms, a near-perfect example of a change in highest and best use — the most profitable, legally permissible use a property can support. For thirty years, the most realistic "use" of a dark, deteriorating landmark hemmed in by historic protections was essentially nothing. Adaptive reuse into a food hall and event center unlocked value that had been frozen for decades, and that shift radiates outward to the parcels around it.

When I appraise a home, the neighborhood section of the report is never an afterthought. Locational influences — walkability, dining, foot traffic, the general sense of whether an area is trending up or down — feed directly into how the market prices a property. For years, the dark Miramar functioned as a mild form of external obsolescence for North Beach: a prominent, visible reminder of stalled momentum right at the district's entrance. Flipping that from dormant to thriving removes a drag and adds an amenity, and both move in the direction of value.

There's also a timing wrinkle that matters more than people realize, especially for estate and divorce work. A retrospective appraisal — the kind used for date-of-death valuations and trust or estate appraisals — values a property as of a specific past date, using only what the market knew then. A North Beach home valued as of a date when the Miramar was still shuttered may carry a measurably different value than the same home valued after the reopening. For attorneys, executors, and CPAs handling these assignments, getting that effective date and the corresponding market conditions right is exactly where a credible, well-supported appraisal earns its keep.

The bottom line

After more than thirty years of a dark marquee, the Miramar is open again, and North Beach has its cornerstone back. For homeowners in the area, that's not just a nice place to grab lunch — it's a meaningful, durable shift in the neighborhood's profile, and the kind of change that thoughtful appraisers track closely.

Frequently Asked Questions

Does a new development or amenity like the Miramar actually affect my home's appraised value? It can, though rarely overnight and rarely in isolation. Appraisers don't assign a dollar figure to "a food hall opened nearby." Instead, we look at what the market does in response — whether comparable sales in the area start showing stronger prices, faster sale times, or fewer concessions after a neighborhood amenity comes online. If the data supports it, that improved desirability shows up in the value. The Miramar reopening is the kind of locational shift worth watching in North Beach over the next several sales cycles.

What is a retrospective (date-of-death) appraisal, and when would I need one? A retrospective appraisal estimates a property's market value as of a specific date in the past, using only the data the market had at that time. The most common reason is a date-of-death valuation for an estate or trust, where the IRS and the courts generally want the value as of the date the owner passed. These are also used in divorce, litigation, and tax matters. Because the effective date drives everything, a North Beach home valued before the Miramar reopened could carry a different supported value than the same home valued after.

How is a professional appraisal different from an agent's market analysis or an online estimate? An online estimate or an agent's comparative market analysis is a useful starting point, but it isn't an independent, USPAP-compliant opinion of value prepared by a licensed appraiser. For estate settlements, divorce proceedings, litigation, tax planning, and lending, those situations typically call for a formal appraisal that's defensible if it's ever questioned by the IRS, a court, or opposing counsel. Independence is the whole point — an appraiser has no stake in the number coming in high or low.

Do I need an appraisal for an estate or a divorce in California? Often, yes — but the specifics depend on your situation, and that's a question for your attorney or CPA. Estates frequently need a date-of-death value for tax reporting and to establish a stepped-up cost basis, and divorcing couples usually need a credible, neutral value to divide a home equitably. An independent appraisal gives both sides and the court a figure they can rely on. I'm happy to coordinate directly with your attorney or accountant on the effective date and scope.

How do you account for a neighborhood that's clearly changing? Carefully, and with data rather than optimism. When an area is in transition, I pay close attention to the most recent comparable sales, current listings and pending sales, and how quickly the market is moving, then apply market-conditions adjustments where the evidence supports them. The goal is always a value that reflects what a buyer would actually pay today — or as of whatever date the assignment calls for — not a guess about where the neighborhood might be headed.

Just Appraisals, Inc. provides independent, USPAP-compliant residential appraisals across coastal Orange County, including San Clemente, Dana Point, Laguna Beach, and Newport Beach. We specialize in date-of-death and estate valuations, divorce and litigation appraisals, and private-fee assignments for attorneys, agents, and homeowners.

Need a credible value — current or retrospective — on a North Beach or South County property? Get in touch.

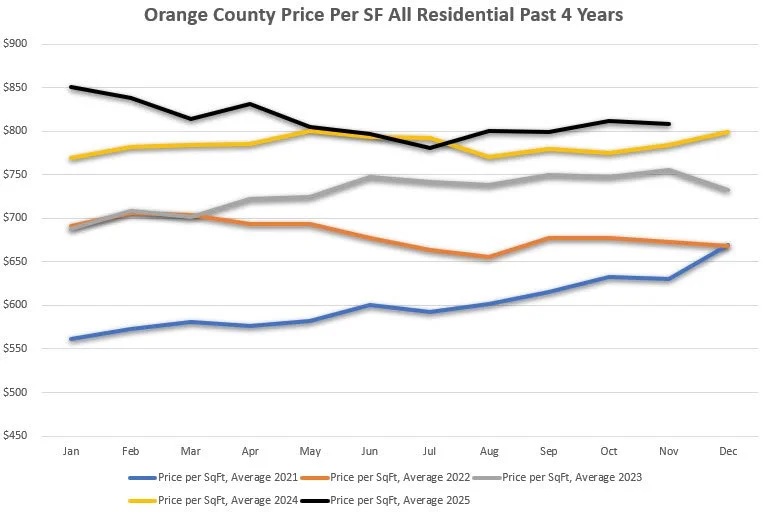

Orange County Price Per Square Foot: A Four-Year Look at the Market

Four years of CRMLS data on Orange County residential pricing — what changed, what held, and what it means for buyers, sellers, and estate planning.

Orange County Price Per Square Foot — All Residential, past 4 years

The chart says a few things clearly. Everything else is context.

We've been tracking Orange County residential price per square foot using CRMLS data since 2022. Four years is enough to separate seasonal noise from actual trend — and to understand where this market actually stands, rather than where the headlines say it does.

2022: The Adjustment Year

Prices started 2022 high and came off through the summer as mortgage rates moved fast. Buyers recalibrated purchasing power. Sellers took longer to adjust expectations. By fall, prices had reset to a more defensible level.

What didn't happen: prices didn't collapse. Orange County's supply constraints and long-term desirability provided a floor. The market corrected; it didn't break.

2023: Stabilization

By 2023, most buyers had accepted the new rate environment. Price per square foot trended upward through the year. Inventory stayed tight, and well-located properties — particularly in coastal south OC communities like Laguna Niguel, Dana Point, and Laguna Beach — continued to command strong numbers.

The market stopped reacting and started settling.

2024: Back to Seasonal Patterns

2024 looked like a normal market. Spring strength, summer softening, modest firming in the fall. Seasonal patterns had returned — which is what you'd expect in a market that's no longer in crisis mode.

For appraisal purposes, 2024 was the first year in a while where comparable sales were straightforward to interpret. The market was behaving rationally again.

2025: Stability at Elevated Levels

The 2025 line sits above all prior years and has held remarkably steady. Sellers have been disciplined on pricing. Buyers are active but selective. Properties in desirable areas — south OC, coastal communities, established neighborhoods in Mission Viejo, Laguna Hills, Aliso Viejo — continue to attract competition.

What we're not seeing is speculation-driven appreciation or panic-driven declines. It's a balanced market, supported by constrained supply and a buyer pool that's adapted to current interest rates.

What This Data Means for Different Situations

Estate and divorce appraisals: The 2022–2023 period created real complexity for date-of-death valuations and divorce appraisals requiring retroactive values. If you need a certified value from that period, the appraiser needs to know the data well enough to reconstruct what was happening month by month in that specific submarket. General countywide trends don't cut it — you need someone who worked in those markets during that period.

Pre-listing appraisals: In a market this stable, pricing discipline matters more than ever. The ceiling on what buyers will pay is real and relatively narrow. A pre-listing appraisal gives you a certified, defensible number to price from rather than a guess based on what the place two streets over listed for.

South OC specifically: Markets in Laguna Beach, Laguna Hills, Lake Forest, Mission Viejo, and San Clemente have their own pricing dynamics within the broader OC trend. Price per square foot countywide can mask significant variation across neighborhoods. Local knowledge — who's buying, what's selling, which comps are actually comparable — is what separates an accurate appraisal from a number pulled from a chart.

Data sourced from CRMLS. Average price per square foot, all residential, Orange County, 2022–2025. Deemed reliable but not guaranteed. Not a substitute for a property-specific appraisal.

Need an appraisal in Orange County? Call Mat directly at (714) 409-6123 or request an appraisal here.

When Is the Best Time to Buy or Sell a Home in Orange County?

our years of CRMLS data shows a clear seasonal pattern in Orange County real estate. Here's what the numbers actually say about timing the market.

Source: CRMLS (Entire California CRMLS). Average price per sf all residential past 4 years.

What the Data Shows

December is the best month to buy. It's not close.

Every single year in the dataset, December recorded the annual low price per square foot:

December 2022: ~$529/sq ft

December 2023: ~$563/sq ft

December 2024: ~$581/sq ft

December 2025: ~$584/sq ft

November typically runs a close second.

On the sell side, the spring market — March through May — consistently produces the highest prices, with averages ranging from roughly $622 to $652 per square foot. That's a seasonal swing of $60 to $70 per square foot between the December trough and the spring peak. On a percentage basis, that's approximately 10 to 11 percent.

On a 1,500 square foot home, that swing is $90,000 to $105,000.

Why December Works for Buyers

Three things converge in late fall and winter that don't happen at other times of year.

Less competition. The spring market brings multiple offers and waived contingencies. November and December are quieter, and that quieter market gives buyers room to negotiate.

More motivated sellers. Anyone still listed in December has usually been on the market for a while. Expectations have adjusted. They don't want to carry the property through the holidays and into a new year.

More days on market. Longer market times translate to more price reductions and more willingness to negotiate on repairs, credits, or terms.

A Note on Price Per Square Foot

Price per square foot is useful as a directional indicator, but it's not the complete picture. The mix of properties selling in winter tends to skew smaller and more modest than the spring luxury market — which can make December look softer than it actually is for any individual property.

That's especially true in south Orange County, where markets like Laguna Beach, Laguna Niguel, Dana Point, and San Clemente carry higher price points year-round and attract a different buyer pool. The seasonal swing in those markets may be less pronounced than the countywide average suggests.

What This Means in Practice

If you're a buyer: late October through December is historically the most favorable window. You won't have the widest selection, but the properties available are more likely to be priced realistically, with sellers who are ready to deal.

If you're a seller: March through May remains the strongest window to list in Orange County. That's when buyer activity peaks and pricing follows.

If you're navigating an estate sale, divorce, or any situation where timing is constrained: the market will do what it does. What matters more than timing is having an accurate, defensible appraisal going in. The seasonal data is useful context — it doesn't override the fundamentals of the individual property.

Data sourced from CRMLS. Average price per square foot, all residential, Orange County, 2022–2025. Deemed reliable but not guaranteed. This is market context, not a substitute for a property-specific appraisal.

Need an independent appraisal in Orange County? Call Mat directly at (714) 409-6123 or request an appraisal here.

Why Property Appraisals in San Clemente Require Local Knowledge

San Clemente's micro-neighborhoods, ocean view premiums, and custom home inventory make it one of the more complex appraisal markets in south Orange County.

Mat on a family outing in Orange County, CA

San Clemente looks like one market. It isn't.

In 24 years of appraising properties throughout Orange County, Mat has covered San Clemente more than most. Just Appraisals Inc. maintains an office in San Clemente — and that proximity matters, because this is one of the more nuanced appraisal markets in south OC.

Here's why.

Micro-Neighborhoods with Real Value Differences

San Clemente isn't a market you can price by zip code. Southeast San Clemente — beach-adjacent properties near T Street, Poche Beach, and the pier — carries a completely different value profile than the golf communities and inland neighborhoods further from the water. Ocean view premiums can run 10 to 20 percent above comparable non-view properties, and the range of those premiums depends on actual line-of-sight, elevation, and proximity — not just neighborhood.

Getting a view premium right requires knowing which comparables are actually comparable. A property in Talega is not the same market as one in the Cotton Point Estates area, even if the distance between them is less than a mile.

Estate and Divorce Appraisals in San Clemente

San Clemente sees a significant volume of estate and divorce appraisals — both because of its established, older neighborhoods and because the properties tend to carry real complexity. Custom builds, significant lot variation, ocean views, and a mix of newer planned communities and legacy homes mean you can't approach these appraisals formulaically.

For estate purposes — date of death valuations, inherited property, step-up in basis — getting a retroactive value right in a market like San Clemente requires more than pulling recent sales. It requires understanding what was driving value at a specific point in time in this specific submarket. The 2022 rate-adjustment period, for example, hit different price points and property types differently across south OC. A general countywide trend line won't tell you what a particular home in San Clemente was worth in a particular month.

The South OC Coastal Connection

San Clemente doesn't sit in isolation. It shares a comparable sales pool with Dana Point to the north and the San Diego coastal corridor to the south. In estate and divorce proceedings, properties in San Clemente are sometimes compared to Laguna Niguel and Laguna Beach depending on price point and property type.

An appraiser who doesn't work south OC regularly won't have an accurate feel for those relationships — which comparables to use, which to set aside, and how the subject property's ocean view, lot size, or location within San Clemente changes the analysis.

Pre-Listing Appraisals in a Complex Market

If you're selling a home in San Clemente, a pre-listing appraisal is particularly valuable. In a market with this much variation in neighborhood, view, and property type, relying solely on an agent's price opinion — or on what a similar-looking home a few streets over listed for — can cost you in either direction.

An accurate pre-listing appraisal gives you a certified, defensible number to price from. In a market where the difference between a view property and a non-view property can be $100,000 or more, getting that number right matters.

Why Local Experience Is Not Optional Here

Some markets are forgiving. San Clemente isn't one of them. The micro-neighborhood variation, the view premium complexity, the mix of property types, and the submarket relationship to the broader south OC and San Diego coastal corridor all require an appraiser who has worked these properties — not just someone who can pull comps from a database.

Mat has been appraising properties in San Clemente, Dana Point, Laguna Beach, Laguna Niguel, and the surrounding south OC markets for over 24 years. Every appraisal carries Mat's signature — his experience, his standards, his word.

Just Appraisals Inc. serves San Clemente and all of south Orange County — estate, divorce, and pre-listing appraisals. Call (714) 409-6123 or request an appraisal here.

5 Things People Get Wrong About VA Appraisals in Orange County

Common misconceptions about VA appraisals clarified by a 24-year Orange County appraiser. What buyers, sellers, and agents need to know before closing.

VA Appraisal Orange County Real Estate Appraiser

VA appraisals generate more confusion than almost any other part of the home buying process. Buyers, sellers, and agents come in with assumptions — some passed along by other agents, some from prior transactions, some just from the internet — that turn out to be wrong. Here's what actually applies.

Myth 1: Utilities Need to Be On During the VA Appraisal

They don't. The VA handbook does not require the appraiser to turn on or verify utilities. This gets conflated with home inspection standards, but appraisers aren't inspectors — the scope is different. If a lender or agent is insisting on utilities being active for the appraisal specifically, that's either a lender overlay or a misunderstanding, not a VA requirement.

Myth 2: Water Heaters Must Be Double-Strapped

The VA has no state-specific requirements like double-strapping water heaters. This is a California building code and insurance concern — and lenders sometimes add it as their own requirement on top of VA standards — but it is not a condition that VA appraisers are required to impose. An appraiser who makes a report subject to double-strapping is going beyond what the VA actually mandates, and can be reprimanded for it.

Myth 3: Smoke and CO Detectors Are Required

Not a VA nationwide requirement. Local building codes and individual lenders may require smoke and carbon monoxide detectors — and you should have them regardless — but VA appraisers are not supposed to condition reports on their installation unless a specific lender requirement is driving it. The distinction matters: VA minimum property standards and lender overlays are not the same thing.

Myth 4: Flaking and Peeling Paint Doesn't Matter

This one runs the other direction — peeling paint actually is a problem, and it sometimes gets overlooked by sellers who assume VA appraisers don't look for it. Flaking or peeling paint is a VA minimum property requirement. It needs to be scraped and repainted before closing, and paint chips on the ground need to be removed. This applies to interior and exterior surfaces. In older Orange County homes — and there are plenty of them, particularly in south OC cities like San Clemente, Dana Point, and older Laguna Beach neighborhoods — lead paint is a real concern and one the VA takes seriously.

Myth 5: VA Appraisals Are Stricter Than Conventional

Not necessarily. VA and FHA both have minimum property requirements that conventional loans don't impose — the peeling paint rule is one example. But FHA actually has slightly more requirements than VA in several areas. And in practice, after 24 years of working across Orange County appraisals, the VA process tends to run smoother than people expect. The intent of VA minimum property standards is to protect veterans purchasing a safe, livable home — not to create hurdles.

A Note on South Orange County and VA Financing

San Clemente, Dana Point, and the communities adjacent to Camp Pendleton see a significant volume of VA-financed transactions. Active-duty buyers and veterans make up a meaningful share of that market — which means agents and sellers in those areas encounter VA appraisals more often than in most parts of OC.

Understanding what VA standards actually require (versus what gets passed along informally) can keep transactions from derailing over non-issues — and can also ensure real requirements like paint condition aren't overlooked until the last minute.

Sources: VA Lender's Handbook, Chapter 11 — Appraisal Requirements and Procedures.VA Lender's Handbook (benefits.va.gov)

A note on Just Appraisals Inc.: We specialize in non-lending appraisals — estate, divorce, pre-listing, and PMI removal. We don't conduct VA lending appraisals. But after 24 years appraising Orange County properties across every type of transaction, we know what separates fact from assumption in the appraisal process. If you have questions about estate, divorce, or pre-listing appraisals in OC, call Mat directly at (714) 409-6123 or request an appraisal here.

How to Remove PMI in Orange County — and Why an Appraisal Is the Key

If you bought in Orange County in the last few years, your home's value may have increased enough to cancel PMI. Here's how the appraisal process works.

A typical house in Orange County — Just Appraisals, Inc.

If you're paying private mortgage insurance every month, there's a good chance you don't have to be anymore.

In Orange County — particularly in south OC markets like Laguna Niguel, Mission Viejo, Lake Forest, Laguna Hills, and Aliso Viejo — property values have increased substantially since 2020. Many homeowners who put down less than 20% when they bought are now sitting on enough equity to cancel PMI entirely. The monthly savings are often $100 to $300 or more depending on loan size.

Here's what you need to know.

What PMI Is and Why It Exists

Private Mortgage Insurance protects your lender, not you. If you put down less than 20% at purchase, your lender takes on more risk — and PMI covers that risk in case of default. It typically adds 0.5% to 1.5% of your loan amount per year to your monthly payment.

You don't have to pay it forever.

The Two Ways PMI Ends

Automatic cancellation — By federal law (the Homeowners Protection Act), your lender is required to automatically cancel PMI when your loan balance reaches 78% of the original purchase price. That means you've paid down to 22% equity based on what you paid for the home. This happens on its own; no action required.

Requested cancellation — Here's the more useful option. You can request PMI removal once your loan balance reaches 80% of the current appraised value — not the original purchase price. In a market where values have risen, this threshold is often reachable years before the automatic cancellation point.

That's where an independent appraisal comes in.

How the Process Work

Once you believe your home has appreciated enough to reach 20% equity at current market value, the process is straightforward:

Contact your lender. Ask specifically about their PMI removal requirements. Different servicers have slightly different documentation procedures and minimum timelines.

Order an independent appraisal. Your lender will require a formal, certified appraisal — not an automated valuation, not a Zillow estimate. Just Appraisals Inc. conducts PMI removal appraisals throughout Orange County, including all south OC cities.

Submit a formal request. Send the appraisal to your lender with a written request for PMI cancellation and any required supporting documentation.

Your lender reviews and cancels PMI if the current appraised value supports the 80% loan-to-value threshold.

Why Orange County Homeowners Are in a Strong Position Right Now

From 2020 through 2024, Orange County residential values increased significantly across the board. A homeowner who purchased in Mission Viejo, Lake Forest, Laguna Hills, or Laguna Niguel in 2020 or 2021 with a 5% or 10% down payment may now have well over 20% equity based on current market value — even before accounting for four-plus years of mortgage payments made.

The math moves faster than most people expect. On a $700,000 purchase with 10% down, a 15% increase in appraised value substantially closes the gap to 20% equity. In some south OC markets, appreciation since 2020 has been considerably higher.

The only way to know for certain is to get the appraisal.

What It Costs vs. What You'd Save

A PMI removal appraisal from Just Appraisals Inc. runs $550 to $900 depending on property type and square footage. If PMI cancels, you might be saving $150 to $250 per month — meaning the appraisal pays for itself in three to five months, and saves you thousands in the years that follow.

It's one of the more straightforward financial decisions in real estate: pay once to confirm a current value, stop paying a monthly fee you no longer owe.

Ready to find out if your home's value supports PMI removal? Call Mat directly at (714) 409-6123 or request an appraisal here. Most inspections are scheduled within 72 hours.